The Space Alchemy: Exposing the Observability Paradox and the Streetlight Effect in the $1.77T SpaceX IPO

The global capital markets are currently transfixed by the dazzling trajectory of the upcoming Space Exploration Technologies Corp. public offering. Under the trading symbol $SPCX, the company seeks to execute the largest initial public offering in corporate history, aiming to raise $75 billion gross by offering 555,555,555 Class A common stock base shares at a targeted price of $135.00 per share. The resulting market capitalisation positions the entity at a staggering implied valuation of approximately $1.77 trillion.

Beneath the current wave of retail mania—underpinned by absolute devotion to the founder and amplified by an unusually high 30 per cent retail allocation carved from a public float constituting a mere 4 per cent of total outstanding shares—lies an architectural optical illusion. Traditional equity research stands divided; whilst speculative retail momentum demands a premium based on blind faith, traditional institutional valuation models discount the target pricing by up to 48 per cent, citing unproven monetisation pathways, and structural opacity.

To approach an offering of this magnitude like a true forensic diagnostician—a Strategic Bloodhound—one must deliberately look away from the flashing lights of the rocket pads and conduct an Organisational CT Scan on the raw ledger. When one strips away the narrative hype, the prospectus exposes an extraordinary structural asymmetry designed to harvest deep public capital whilst completely immunising management from public market accountability.

1. The GAAP Optical Illusion: Purchasing the Un-Bookable Asset Engine

The primary friction point for any rational capital allocator reviewing the prospectus is the severe, mathematical disconnect between the market purchase price and the tangible assets recorded on the balance sheet. The accounting mechanics map out an immediate redistribution of wealth across the share pool that defies traditional public equity expectations:

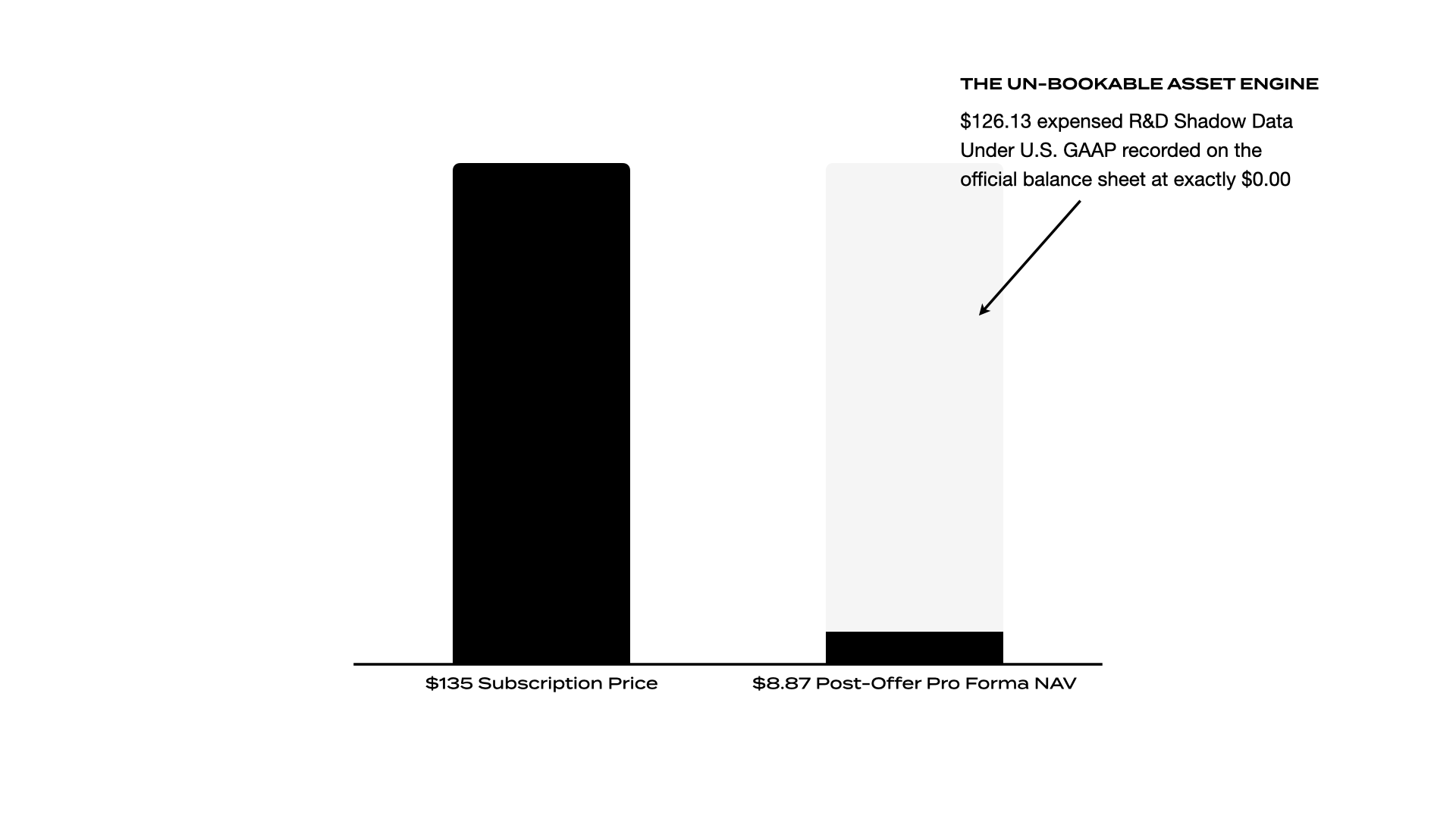

The Premium Entry Price: Public investors are required to pay $135.00 per share.

The Underlying Asset Baseline: Prior to the public cash injection, the company's historical net assets yield an underlying pro forma net asset value (NAV) of a meagre $3.32 per share.

The Post-IPO Equilibrium: After pooling the massive $74.4 billion in net public cash straight into the general corporate treasury, the as-adjusted pro forma NAV crawls up to exactly $8.87 per share.

The prospectus does not conceal this stark asymmetry; it explicitly categorises the remaining $126.13 per share gap as immediate “dilution in pro forma net asset value per share to new investors”. Every new incoming investor is effectively swapping $126.13 per share for pure, on-paper nothingness.

The Dilution Ledger

Investor Subscription Price: $135.00

Post-Offering Pro Forma NAV: $8.87

Immediate Paper Dilution: $126.13

Figure 1: The SpaceX Dilution Ledger and the GAAP Observability Gap

However, a deeper diagnostic scan reveals that this extreme dilution is not a simple accounting penalty, but rather a vivid demonstration of the Observability Paradox in deep-tech asset classes. Under modern financial reporting standards (U.S. GAAP), standard corporate accounting rules impose a structural “Streetlight Effect”. Because companies are legally restricted from capitalising long-term developmental milestones on the balance sheet, SpaceX is mandated to immediately expense its ultra-heavy innovation costs through the statement of operations.

When the firm expenses $3+ billion developing its Starship launch system or $5+ billion building out advanced xAI compute models and infrastructure in a single fiscal year, those billions are instantly wiped from the asset ledger. Consequently, decades of revolutionary engineering intellectual property, flight data, and frontier model weights are recorded on the official balance sheet at exactly $0.00.

When an investor pays $135.00 per share, they are not buying a fractional stake in existing physical steel, concrete, or solar arrays. They are paying an extraordinary premium to bypass the regulatory blindness of standard corporate accounting and purchase an un-bookable operational capacity.

2. Deconstructing the Science Fiction Narrative: The AI Cash Burn

To evaluate whether this un-bookable engine can ever manufacture monetisable tokens fast enough to justify a valuation premium reliant on exponential, flawless execution, one must isolate the underlying corporate segment metrics. The ledger exposes a highly profitable terrestrial connectivity monopoly that is being structurally leveraged to fund a speculative, hyper-capital-intensive leap into an orbital data economy.

The reportable segments present two entirely separate financial dimensions:

Consolidated Segment Performance (FY 2025)

Whilst the Starlink consumer and enterprise engine operates beautifully—generating strong segment income from operations—the newly integrated AI segment is a massive cash incinerator. The AI segment dragged company-wide operations down to a consolidated net loss of $4,937 million in 2025, driven by a rapid, uncapitalised CapEx scale-up from $463 million in 2023 to $12,727 million in 2025.

As Wall Street legend Steve Eisman succinctly summarised the situation on CNBC:

“What I love about the S-1 is that it reads like a science fiction novel. It really does.”

For the experienced asset allocator, this structural configuration reveals a familiar operational playbook. The architect of this offering possesses a documented track record of utilising long-duration, narrative-driven technological horizons—most notably demonstrated via historical capitalisation cycles within the electric vehicle sector—to command immense capital premiums from an inelastic retail investor base long before the underlying technology achieves commercial maturity. Furthermore, the alleged subsequent retrofitting of digital agreements to manage downside liability underscores a broader corporate strategy: leveraging absolute public market devotion to fund highly speculative infrastructure, whilst structurally shielding the issuer from legal volatility, operational compliance metrics, and financial downside when execution timelines inevitably expand.

The primary structural pathogen hidden in the prospectus narrative lies in the company's definition of its Total Addressable Market (TAM). SpaceX claims a quantifiable TAM of $28.5 trillion, of which an astonishing 85 per cent ($26.5 trillion) is tied entirely to artificial intelligence applications and enterprise infrastructure.

To put this macro projection into perspective: a $28.5 trillion addressable market implies that a single corporate entity intends to capture nearly 30 per cent of the entire economic output of planet Earth—and plans to do it by selling highly commoditised, non-differentiable Large Language Models (LLMs) rather than core orbital launch systems.

To achieve those metrics, the firm would effectively need to automate the cognitive output of the entire global working population—all 3.5 billion of us.

Conveniently, the prospectus reveals that the founder's multi-trillion-dollar equity bonus tranches trigger only if he establishes a permanent Mars colony of at least one million inhabitants. Removing a million workers from the terrestrial tax base may satisfy interplanetary ambitions, but it represents an unprecedented operational risk for public market investors who require near-term cash generation over long-term cosmic execution velocity.

3. The Synthetic Index Engine: Nasdaq’s Mandatory Institutional Conduit

To ensure the success of this capital harvest despite severe institutional scepticism, the structural layout extends far beyond the corporate bylaws of the firm. It has required an extraordinary regulatory realignment of the public market infrastructure itself. To facilitate the immediate inclusion of SpaceX into major benchmarks like the Nasdaq-100, Nasdaq has adjusted its historical “seasonin” and weighting rules specifically to accommodate megacap private companies launching initial public offerings.

This synthetic demand engine operates via four radical modifications to standard index methodology:

The “Fast Entry” Protocol: Nasdaq has compressed the mandatory seasoning period—the traditional window a security must trade on the open exchange before index admission—from the historic three months down to just 15 trading days.

The Eradication of Minimum Free Float: Historically, an enterprise required a minimum 10 per cent public float to qualify for index inclusion. Nasdaq has scrapped this requirement entirely to accommodate SpaceX, which is listing with a tightly restricted public float of just 4 per cent of total shares.

The Low-Float Weighting Multiplier: To prevent a highly constrained float from resulting in an artificially muted index presence, Nasdaq has introduced a protocol applying a corporate threefold (3x) multiplier to the weighting calculation of any listing with a float below 20 per cent.

Aggregated Market Capitalisation Metrics: The index updated its methodology to aggregate unlisted and listed share classes collectively, properly capturing the true scale of the entity's megacap valuation for eligibility tracking.

The net effect of these structural interventions is an intentional systemic siphon. It legally compels passive index trackers, automated exchange-traded funds (ETFs), and institutional portfolios to purchase millions of shares of the company shortly after its trading debut. It creates guaranteed programmatic buying pressure on a low-float asset, whilst allowing insiders to preserve absolute control over corporate direction.

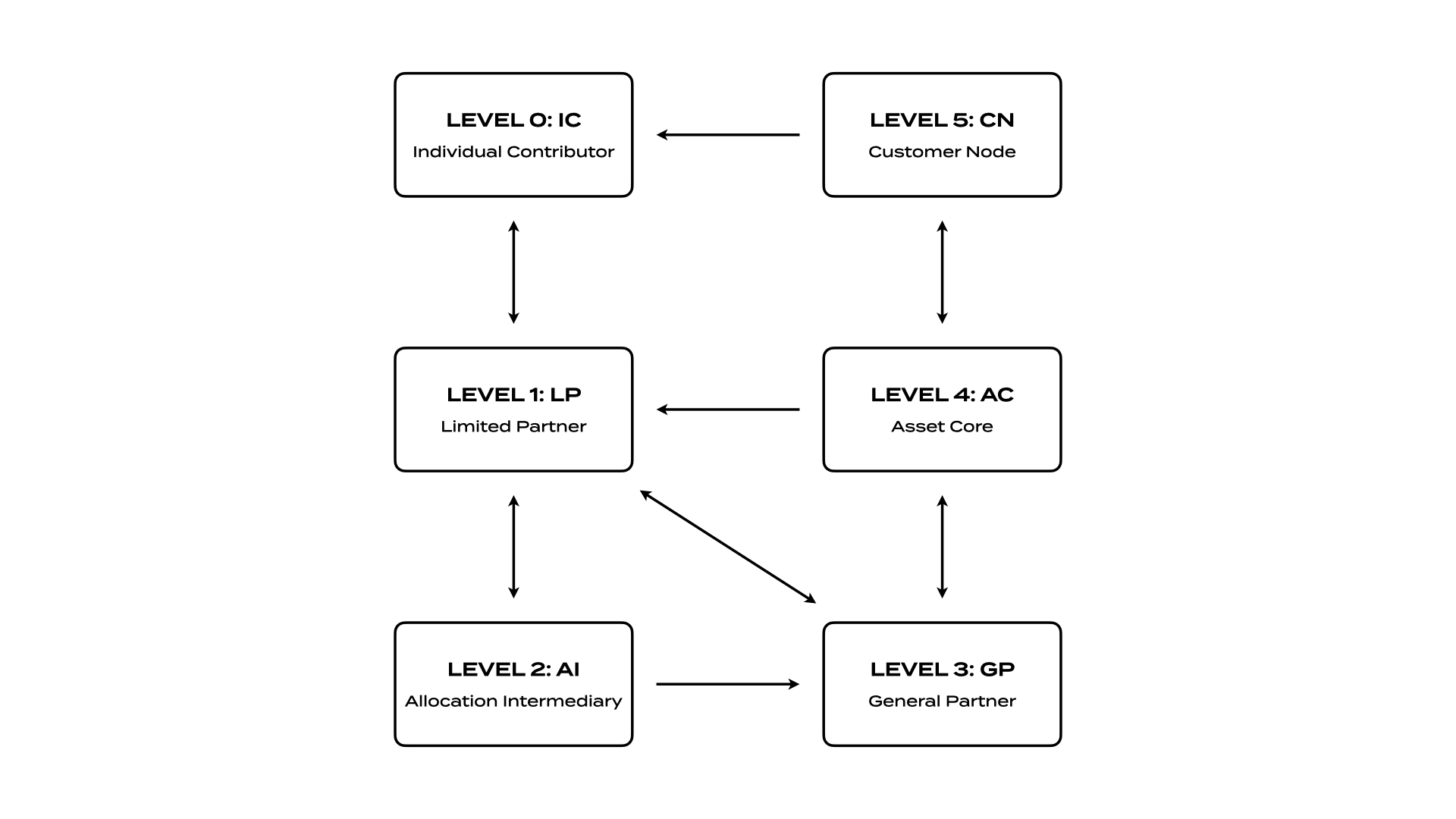

From an end-to-end systems perspective, this programmatic conduit exposes a profound boundary condition within the global capital architecture. To map the transaction flow with absolute topological completeness, a forensic diagnostic cannot merely analyse intermediate institutional intermediary nodes; it must trace the circuit to its primary source of capital energy—Level 0: The Individual Contributor.

Whether that contributor is an ultra-high-net-worth patriarch insulating a multi-generational family office estate, or a self-employed freelancer diligently allocating monthly surpluses to secure a retirement pension thirty years hence, these human lives constitute the absolute foundation underlaying sovereign wealth vehicles, mutual funds, and pension allocators.

Figure 2: End-to-End System Topology - Programmatic Capital Harvesting from Level 0 to the Asset Core

Without the individual contributor, the intermediate institutional layers possess zero sovereign capital to deploy.

Through Nasdaq's strategic optimisation of indexation algorithms, the active intent of the Level 0 contributor is entirely decoupled from allocation reality. The individual savings of a freelancer choosing a broad-market passive vehicle are automatically, invisibly, and systematically funnelled into $SPCX to absorb an asset carrying an immediate 93 per cent paper dilution down to book value. Capital energy is harvested programmatically at the system's boundary, leaving the primary wealth creator with zero control over whether or not their savings are weaponised to underwrite interplanetary software alchemy.

4. The Governance Moat: Architecture of the $53 Billion Firewall

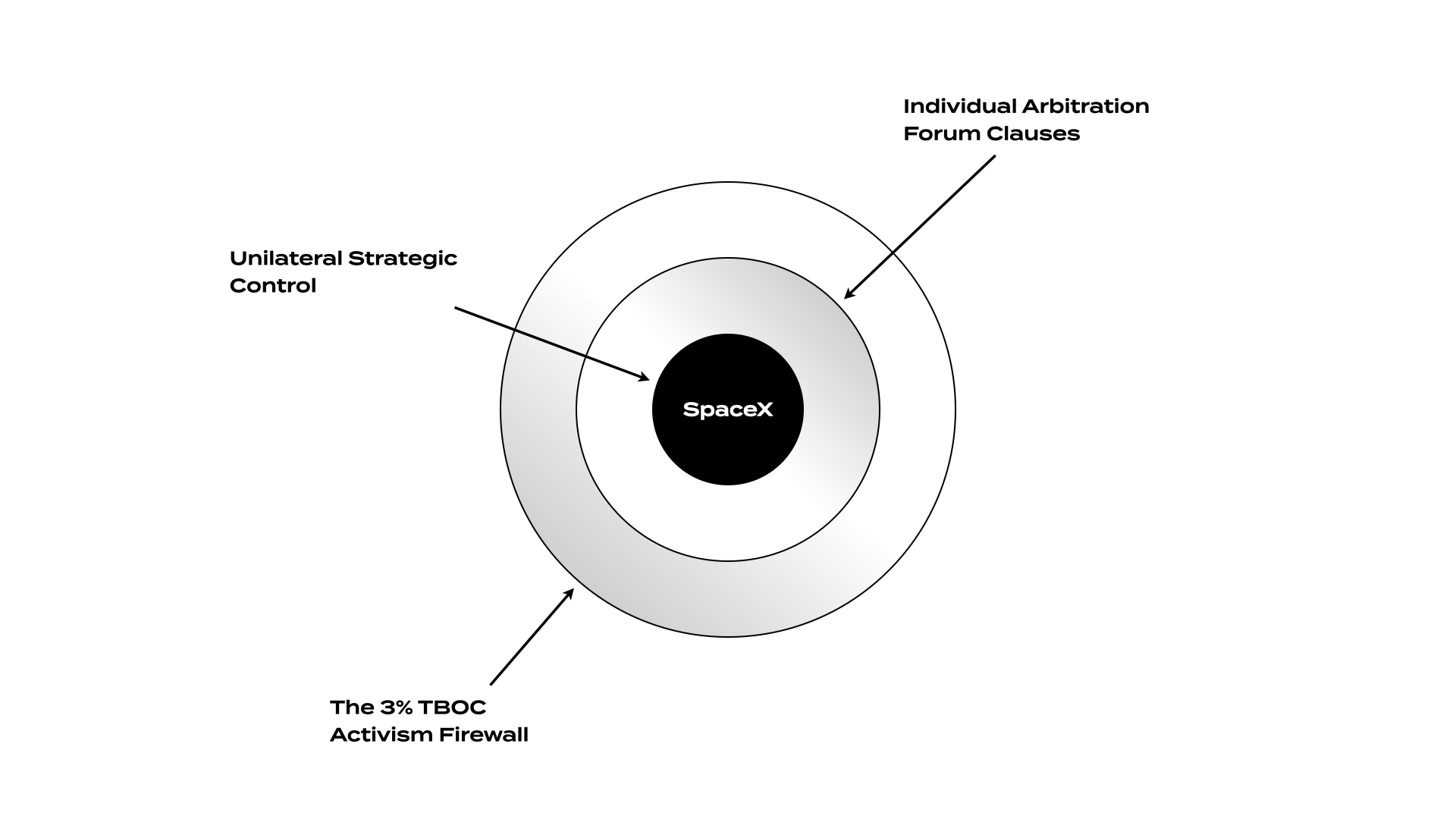

Because the true value of the firm is entirely un-booked and detached from traditional public market parameters, management has pre-emptively engineered an airtight corporate defence mechanism. This structure ensures that traditional public market volatility, quarterly earnings anxiety, or hostile activist shareholders can never legally force them to defend a balance sheet that fails to reflect reality.

The governance framework operates with absolute, clinical insulation through three distinct layers of corporate masonry:

Absolute Voting Concentration: Public retail investors are issued Class A common stock carrying 1 vote per share. However, key long-term insiders hold Class B shares carrying 10 votes per share. This dual-class configuration completely concentrates voting dominance, giving Elon Musk unilateral control over board compositions, corporate opportunities, and strategic capital allocation.

The Activism Firewall (The 3% Rule): Under section 21.552(a)(3) of the Texas Business Organizations Code (TBOC), the bylaws specify that any shareholder or group seeking to submit a proposal or maintain a derivative legal suit must continuously hold at least 3 per cent of the outstanding voting shares of the corporation for six months. At the initial public offering price of $135.00, entering that governance gate requires an insurmountable capital position of approximately $53 billion. Traditional activist pressure is rendered legally impossible.

Class Action Immunisation: The forum selection bylaws explicitly prohibit shareholders from bringing internal corporate disputes as a collective mass action or class action. Every dispute must be adjudicated or arbitrated individually, completely neutralising the legal leverage of minority shareholders.

Zero Income Yield: The asset baseline features an explicit confirmation that the company does not anticipate paying any cash dividends in the foreseeable future, stripping away any income padding to protect investors during prolonged infrastructure development timelines.

Figure 3: Concentric Corporate Architecture - The Three-Layer Insulated Governance Firewall

The Forensic Diagnostic Verdict

The SpaceX offering represents a historic paradigm shift in the structural layout of the public equity markets. It is not a traditional public listing; it is a giant, late-stage venture capital bridge utilising a public equity framework to harvest sovereign-scale liquidity.

Through custom index adjustments, systemic capital siphoning from Level 0 bounds, and strict governance parameters, management has successfully engineered a capital fortress that completely insulates them from public market impatience.

Investors are not buying a standard, asset-backed stock. They are purchasing a highly premium-priced narrative wrapper around an un-bookable operational ecosystem. The ultimate risk is not the immediate paper dilution down to $8.87; it is whether an investor is willing to trust the narrative completely blindly, knowing that eventually mathematics always solves for X, and gravity always wins—even in space.

Like Eisman, I am not a fan.

When an IPO valuation relies on a market built primarily on speculative AI projections and asteroid mining—rather than core rocket engineering—you are not buying a stock. You are buying a very expensive narrative wrapper.

Sometimes, the best clinical diagnostic is simply knowing when to pass.

(Diagnostic Safety Notice: This essay constitutes a purely clinical, forensic analysis of publicly available regulatory disclosures and prospectus documentation for the purpose of architectural evaluation. It is absolutely not financial advice, a market recommendation, or a live investment tip. I provide this explicit clarification to satisfy overzealous compliance gatekeepers, corporate risk algorithms, and any reader who mistakes baseline asset analysis for a securities endorsement. If you choose to swap your capital for space alchemy, that remains a strictly private matter between your broker, your conscience, and your bank account.)